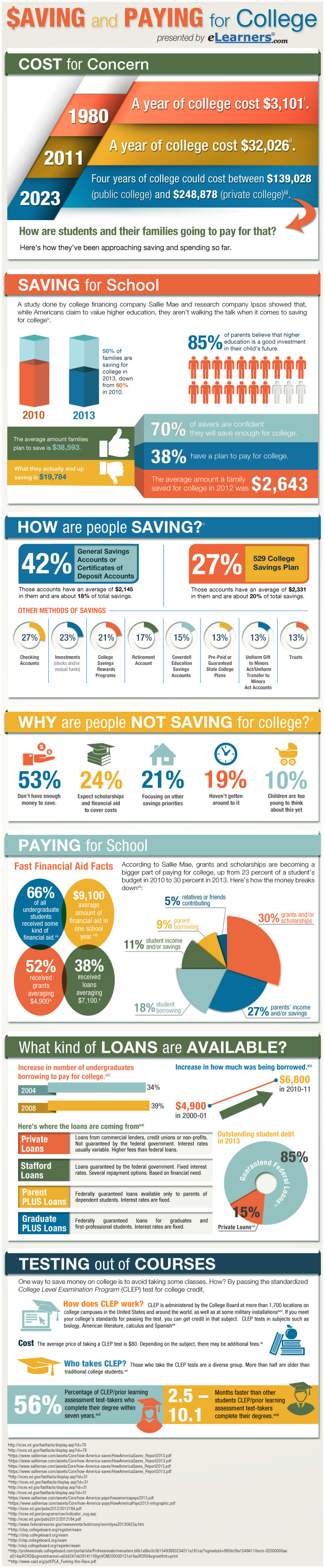

Here's why you should be interested in saving and paying for college. In 1980, a year of college cost $3,101. That would have been $7,759 in 2009-10 dollars, according to a report from the National Center for Education Statistics[i].

In 2011, that cost had skyrocketed to $32,026[ii]. And by 2023? Four years of college could cost between $139,028 at a public college and $248,878 at a private college[iii]. How are students and their families going to pay for that? Here’s how they’ve been approaching how to pay for college so far.

Want to share this image on your site about how to pay for college? Just copy and paste the embed code below:

Saving and Paying for College

A study done by college financing company SallieMae and research company Ipsos showed that, while Americans claim to value higher education, they are not walking the walk when it comes to saving for college[iv].

- 85% of parents believe that higher education is a good investment in their child’s future.

- 50% of families are saving for college in 2013, down from 60% in 2010.

- 70% of savers are confident they will save enough for college.

- The average amount families plan to save is $38,593.

- What they actually end up saving is $19,784.

- Only 38% have a plan to pay for college.

- The average amount a family saved for college in 2012 was $2,643.

How are people saving?

- 42% have general savings accounts or certificates of deposit accounts.[v] Those accounts have an average of $2,145 in them and are about 18% of total savings.

- 27% have a 529 college savings plan, with an average of $2,331 in them. They account for 20% of total savings.

- Other methods of savings include checking accounts (27% of families saving use these), investments such as stocks and/or mutual funds (23%), college savings rewards programs (21%), retirement account (17%), Coverdell Education Savings Accounts (15%), pre-paid or guaranteed state college plans (13%), Uniform Gift to Minors Act/Uniform Transfer to Minors Act accounts (13%) and trusts (13%).

Why are people not saving for college?

- 53%: Don’t have enough money to save.[vi]

- 24%: Expect scholarships and financial aid to cover costs

- 21%: Focusing on other savings priorities

- 19%: Haven’t gotten around to it

- 10%: Children are too young to think about this yet

How to Pay for College

Financial aid helps a lot of students. Sixty-six percent of all undergraduate college students received some kind of financial aid, according to a National Center for Education Statistics study for 2007-2008. [vii]

The average amount of aid was $9,100 [viii]. Fifty-two percent received grants averaging $4,900[ix], while 38 percent received loans with the average amount being $7,100.[x]

According to SallieMae, grants and scholarships are becoming a bigger part of how to pay for college, up from 23 percent of a student’s budget in 2010 to 30 percent in 2013 [xi]. Here’s how the money breaks down[xii]:

- 30% grants and/or scholarships

- 27% parents’ income and/or savings

- 18% student borrowing

- 11% student income and/or savings

- 9% parent borrowing

- 5% relatives or friends contributing

What kind of loans are available?

A 2011 report from the Department of Education’s National Center for Education Statistics showed that the number of undergraduates borrowing to pay for school had increased, from 34 to 39 percent, between 2004 and 2008[xiii]. The amount of money students borrowed in 2010-11 was $6,800, up from $4,900 in 2000-01[xiv]. Here’s where the loans are coming from:

- Private Loans: Education loans from commercial lenders, credit unions or non-profit entities. These loans are not guaranteed by the federal government. Each lender sets its own terms. Interest rates are usually market rate, variable and based on credit history. Fees are generally higher than federal loans.

- Stafford loans: These loans are guaranteed by the federal government. They come with fixed interest rates and a variety of repayment options. There are eligibility requirements. Loan amounts are limited based on factors including total amount borrowed, dependency status and class level. Subsidized Stafford loans are based on financial need. The federal government pays interest on the loan until the student begins repayment and during authorized periods of deferment after that. Unsubsidized Stafford loans are not based on financial need, and students are charged interest for the duration of the loan.

- Parent PLUS loans: These loans are federally guaranteed and available only to parents of dependent students. The interest rate is fixed. Borrowers can’t have bad credit. The amount that can be borrowed is limited to the cost of attending the college minus other financial aid such as grants and scholarships.

- Graduate PLUS loans: These are federally guaranteed loans for graduates and first-professional students. The amount that can be borrowed is limited to the cost of attending the college minus other financial aid such as grants and scholarships. Interest rates are fixed. [xv]

85% of outstanding student debt in 2013 was from guaranteed federal loans. 15% was from private loans.[xvi]

Testing out of courses

One way to save money on college is to avoid taking some classes. How? By passing the standardized College Level Examination Program (CLEP) test for college credit.

How does CLEP work?

CLEP is administered by the College Board at more than 1,700 locations on college campuses in the United States and around the world, as well as at some military installations[xvii]. If you meet your college’s standards for passing the test, you can get credit in that subject.

Subjects you can take CLEP tests for include biology, American literature, calculus and Spanish[xviii]. Depending on the subject, you have 90 minutes to two hours to finish the test [xix]. There are dozens of basic classes that students can potentially test out of and avoid the huge college bills for.

Cost

The average price of taking a CLEP test is $80. Depending on the subject, there may be additional fees.xx

Who Takes CLEP?

Those who take the CLEP tests are a diverse group. More than half are older than traditional college studentsxxi. Some are working people who have professional experience in the subject and are looking to save time and money getting their degree by not having to take elective or introductory courses. Some are active military taking advantage of education benefits. Some are homeschooled students who want to demonstrate their abilities and education. Some are international students seeking credit for what they learned elsewhere.

According to a study done by the Council for Adult and Experiential Learning, 56% of students who take CLEP or a similar prior learning assessment test for credit complete their degree within seven years. And they do it between 2.5 and 10.1 months faster than other students.xxi

Ready for More?

You may also want to read about Accelerated Degree Programs where you can earn a bachelors and masters degree at the same time—talk about bang for your buck!

[i] nces.ed.gov/fastfacts/display.asp?id=76 [ii] nces.ed.gov/fastfacts/display.asp?id=76 [iii] salliemae.com/assets/Core/how-America-saves/HowAmericaSaves_Report2013.pdf [iv] salliemae.com/assets/Core/how-America-saves/HowAmericaSaves_Report2013.pdf [v]salliemae.com/assets/Core/how-America-saves/HowAmericaSaves_Report2013.pdf [vi]salliemae.com/assets/Core/how-America-saves/HowAmericaSaves_Report2013.pdf [vii] nces.ed.gov/fastfacts/display.asp?id=31 [viii] nces.ed.gov/fastfacts/display.asp?id=31 [ix] nces.ed.gov/fastfacts/display.asp?id=31 [x] nces.ed.gov/fastfacts/display.asp?id=31 [xi] salliemae.com/assets/Core/how-America-pays/howamericapays2013.pdf [xii] salliemae.com/assets/Core/how-America-pays/HowAmericaPays2013-infographic.pdf [xiii] nces.ed.gov/pubs2012/2012184.pdf [xiv] nces.ed.gov/programs/coe/indicator_cug.asp [xv];nces.ed.gov/pubs2012/2012184.pdf [xvi] federalreserve.gov/newsevents/testimony/vermilyea20130625a.htm [xvii] clep.collegeboard.org/register/exam [xviii] clep.collegeboard.org/exam [xix] clep.collegeboard.org/exam [xx] clep.collegeboard.org/register/exam [xxi]professionals.collegeboard.com/portal/site/Professionals/menuitem.b6b1a9bc0c5615493883234011a161ca/?vgnextoid=980dcf9a10494110vcm-02000000aaa514acRCRD&vgnextchannel=a0dd247eb2814110VgnVCM200000121a16acRCRD&vgnextfmt=print [xxii] cael.org/pdf/PLA_Fueling-the-Race.pdf